Money is such a complicated subject, isn’t it?

It’s emotional, tied to our sense of security, and—whether we admit it or not—often dictates how much freedom we actually have in life.

But here’s the hard truth: most people don’t stay stuck financially because of bad luck. They stay stuck because of daily habits that quietly eat away at their long-term potential.

I’ve seen it in my counseling work and in conversations with clients who come to me, not only about relationships, but about the stress money puts on them. And it’s almost always the same patterns that separate those who climb out of the lower middle class from those who stay there.

Let’s dig into the seven daily habits that quietly hold people back from ever building wealth.

1. Living for short-term comfort

Do you reach for instant gratification more often than not?

It might look like buying takeout multiple nights a week, picking up small impulse purchases every time you go to the store, or upgrading your phone even though the old one works just fine.

The problem here is not the individual purchase—it’s the pattern. When daily spending is driven by comfort or convenience, savings get pushed aside.

I once had a client who admitted she ordered coffee delivery every morning. She laughed it off as “just a few bucks,” but when we added it up, she was spending nearly $2,000 a year on lattes.

That’s not a judgment—coffee can bring joy! But when small comforts turn into daily financial leaks, they rob us of bigger opportunities like investing or paying down debt.

Psychologist Daniel Goleman once noted, “The ability to delay gratification is a master skill, a triumph of the reasoning brain over the impulsive one.” This couldn’t be truer when it comes to wealth. Those who can delay pleasure and prioritize future rewards are the ones who eventually have the freedom others envy.

2. Avoiding financial literacy

Money feels overwhelming for many people, so they avoid dealing with it. They don’t track their spending. They never learn about investing. They assume budgeting is for people who are “good with numbers.”

But here’s the truth: financial literacy is a skill, not an inborn trait. The more you avoid it, the more powerless you remain.

Warren Buffet put it bluntly: “The more you learn, the more you earn.” Even reading one book on personal finance or listening to a podcast while commuting can shift your mindset. Wealth doesn’t come to those who stay ignorant—it comes to those who take ownership of their financial education.

And here’s the encouraging part: you don’t need an MBA. Just start small. Apps now automatically categorize spending. Online courses can walk you through the basics of investing. Even spending ten minutes a day learning about money compounds into confidence.

I’ve seen couples who argued constantly about bills completely transform once they started sitting down weekly to review their expenses together. They didn’t suddenly make more money—but by becoming financially literate, they learned how to make the money they had work for them.

3. Relying on one source of income

A lot of people in the lower middle class depend entirely on a single paycheck. And to be clear—there’s nothing wrong with honest work. But relying only on one stream of income is risky. One job loss, one health crisis, and everything collapses.

I once worked with a couple who lived paycheck to paycheck for years, despite both of them working full time. Their breakthrough came when they realized they needed to diversify.

She started a side business selling handmade crafts online, and he took on occasional consulting gigs. Within two years, they had built a financial buffer they never thought possible.

And diversification doesn’t always mean starting a business. It could mean investing in dividend-paying stocks, renting out a spare room, or even monetizing a skill like tutoring.

It’s not about hustling yourself into exhaustion. It’s about building resilience. As Tony Robbins has said, “It’s not about resources, it’s about resourcefulness.” Wealthy people rarely rely on just one stream of income—and that’s no accident.

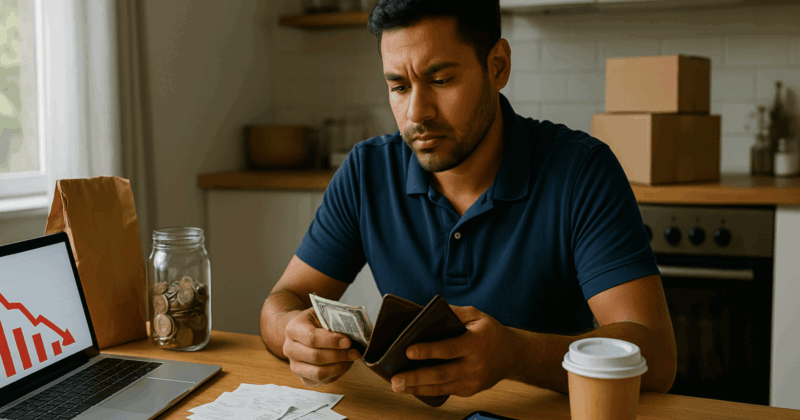

4. Treating credit like free money

Credit cards can be a powerful tool—but only if you know how to use them. Unfortunately, too many people swipe without thinking and carry balances that drain their finances.

High-interest debt is like a leaky bucket. No matter how much money you pour in, it slips away faster than you can save it.

Research from the Federal Reserve shows that the average credit card interest rate is over 20%. That means if you’re carrying a $5,000 balance, you’re paying more than $1,000 a year just in interest. Imagine what that money could do if it were invested instead.

I’ll never forget a woman I worked with who said, “I don’t understand why I’m broke, I make decent money.” When we looked closer, she had six credit cards, all maxed out. She was working to pay interest, not to build wealth.

Credit isn’t the enemy. But using it daily without intention is. When you start treating credit as a tool rather than an income supplement, your financial picture changes completely.

5. Surrounding yourself with the wrong influence

Maya Angelou once said, “You are the sum total of everything you’ve ever seen, heard, eaten, smelled, been told, forgot—it’s all there.”

The same goes for your financial habits. If your circle normalizes overspending, debt, or living for the weekend, you’ll unconsciously adopt those patterns too.

This is why peer groups matter so much. I’ve watched people completely transform their money mindset simply by shifting who they spend time with. Start hanging around people who talk about investments instead of only gossiping about sales. Follow creators who share financial tips instead of influencers flaunting luxury hauls.

One client of mine used to meet friends every Friday at a fancy restaurant. It drained her budget and left her anxious each month. When she switched to inviting friends for potluck dinners at home, not only did she save money, but she also deepened her connections. Small shifts in influence have huge ripple effects.

6. Complaining instead of problem-solving

Here’s one I see all too often: people who spend their evenings complaining about how unfair the system is, how hard it is to get ahead, or how “people like us will never be rich.”

Now, there’s truth in the fact that the system isn’t fair. But staying stuck in a victim mindset doesn’t change anything. It drains energy that could be used to actually move forward.

Steven Covey, in his classic The 7 Habits of Highly Effective People, wrote: “I am not a product of my circumstances. I am a product of my decisions.”

I know someone who used to gripe daily about their low-paying job. But when asked if they’d applied for higher-paying positions or sought training, the answer was always no. Complaining feels like action—but it isn’t.

Every day you complain is a day you don’t act. Wealthy people face challenges too, but the difference is they channel that frustration into solutions, not cycles of negativity.

7. Ignoring health and well-being

Looking back, this one probably deserved a higher spot on the list. Anyway, it’s hard to build wealth if you’re constantly dealing with poor health. And yet, many people neglect daily exercise, eat cheap junk food, or avoid doctor visits to “save money.”

Here’s the paradox: poor health is far more expensive in the long run. Medical bills, lost work time, and reduced energy all chip away at financial potential.

I had a client who worked 60-hour weeks but ignored her health completely. When she eventually burned out and had to take unpaid leave, she realized the cost of neglecting her well-being was greater than the cost of preventive care would have been.

As Michelle Obama has said, “We need to do a better job of putting ourselves higher on our own ‘to do’ list.” If you’re not investing in your health daily—whether that’s through walking, eating better, or managing stress—you’re sabotaging not just your well-being but your wealth-building capacity too.

Final thoughts

If you spotted yourself in any of these habits, don’t panic. Awareness is the first step toward change.

What matters isn’t that you’ve made mistakes—it’s that you’re willing to break patterns. None of these habits are permanent, and all of them can be shifted with consistent effort.

And here’s the hopeful part: small changes compound. A little more financial literacy, one healthier meal, a single side income project—these are the building blocks of long-term wealth.

The lower middle class isn’t a life sentence. But staying there is almost guaranteed if these habits remain on autopilot.

So the real question is, which of these are you ready to let go of today?

- Preferring solitude over constant socializing is a subtle sign of these 7 unique traits - November 7, 2025

- 7 things in life you should always keep to yourself no matter how comfortable you feel around someone - November 7, 2025

- 10 phrases people with poor social skills often use in everyday conversation - November 7, 2025